How to Use Out of Network Therapy Benefits: Complete Guide to Superbills and Reimbursement

Finding the right therapist is one of the most personal and important decisions in your mental health journey. Being limited to a narrow list of in-network providers can mean settling for a therapist who is not the right fit simply because better options are out of network. Out of network therapy benefits solve this problem by allowing you to see any licensed therapist and still receive partial insurance reimbursement. Understanding exactly how these benefits work — and specifically how to use superbills — unlocks access to the best therapist for your needs rather than just the nearest available in-network option.

Disclaimer: Insurance benefits vary significantly by plan. Always verify your specific out of network coverage before beginning therapy. This content is for educational purposes only.

What Are Out of Network Therapy Benefits?

Out of network benefits allow you to receive services from healthcare providers who do not have a contract with your insurance company and still receive partial coverage. For therapy specifically, this means you pay the therapist’s full fee upfront, then submit a claim to your insurance company and receive reimbursement for a percentage of the covered amount.

The key distinction from in-network care is the payment sequence and the reimbursement percentage. In-network, your insurance pays the provider directly and you pay only your copay or coinsurance. Out of network, you pay everything upfront and insurance reimburses you later — typically at a lower percentage than in-network coverage. Despite the additional administrative steps, out of network benefits can make excellent therapy genuinely affordable for many patients.

Not all insurance plans include out of network mental health benefits. HMO plans typically do not. PPO and POS plans usually do. The first step before pursuing out of network therapy is calling your insurance company to confirm whether your plan includes out of network mental health benefits and exactly what those benefits are. Read our guide on How to Find a Therapist That Takes Your Insurance if you prefer to work within your network first.

Questions to Ask Your Insurance Company Before Starting

Call the member services number on your insurance card and ask these specific questions before committing to out of network therapy. Does my plan have out of network mental health benefits? What is my out of network deductible for mental health services? What percentage of the allowed amount does my plan pay after the deductible — this is called coinsurance? What is the allowed amount for outpatient psychotherapy in my plan? Is there a maximum number of sessions covered per year for out of network? Do I need prior authorization for out of network mental health services? What is the process for submitting out of network claims?

Getting answers to all of these questions before your first appointment prevents unpleasant financial surprises. Record the name of the representative you spoke with, the date, and the specific answers provided — this documentation protects you if there are disputes about coverage later.

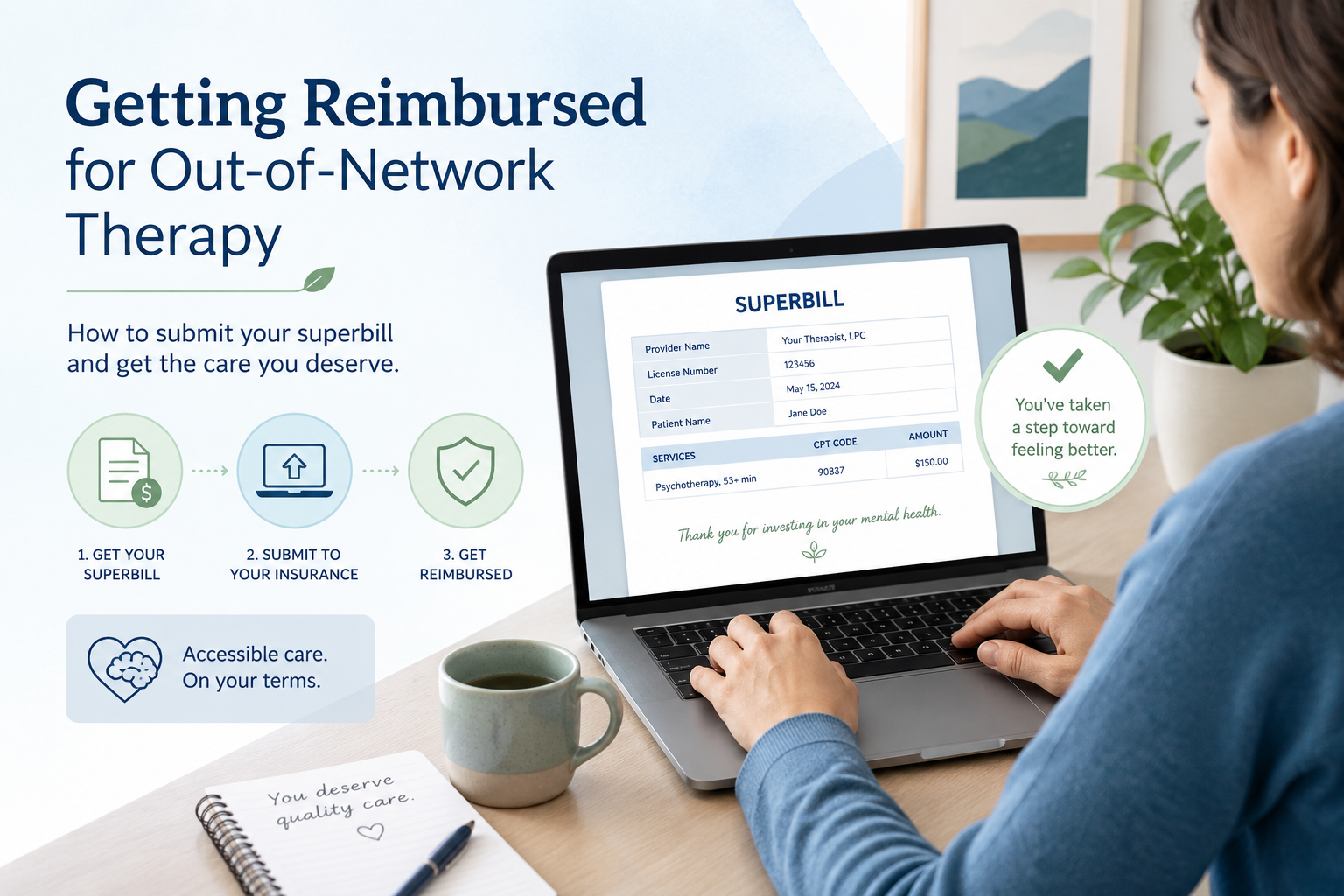

What Is a Superbill and Why Does It Matter?

A superbill is the essential document that makes out of network reimbursement possible. It is a detailed receipt from your therapist that contains all the information your insurance company needs to process an out of network claim. Think of it as a combination of a receipt and a medical claim form that your therapist generates on your behalf.

A properly formatted superbill contains the therapist’s name, license type, and license number, their National Provider Identifier number (NPI), their practice address, the diagnosis code (ICD-10) describing your mental health condition, the procedure code (CPT) describing the type of session, the date of service, the fee charged, and your name and insurance information.

Without a properly formatted superbill, your insurance company cannot process the out of network claim. Before beginning therapy with an out of network provider, confirm they are familiar with providing superbills and ask to see a sample. Most therapists who work with out of network patients have a standard superbill format they provide routinely. For context on understanding the codes that appear on superbills, see our guide on What is a Therapy Copay and How Does It Work.

Step by Step — How to Submit an Out of Network Claim

After each therapy session or at the end of each month, request a superbill from your therapist. Some therapists provide them automatically after each session while others provide monthly compilations — clarify the schedule with your therapist at the beginning of treatment.

Once you have your superbill, log into your insurance company’s member portal online. Most major insurers have a claim submission section where you can upload the superbill directly. Some insurers still require paper submissions — call member services if you cannot find the online submission option.

When submitting, you will typically need to complete a brief claim form in addition to uploading the superbill. This form captures your contact information, the provider’s information, and banking details if you want direct deposit reimbursement rather than a check.

Processing time varies by insurer — typically 2 to 4 weeks for electronic submissions and longer for paper submissions. You will receive an Explanation of Benefits showing how the claim was processed, what the allowed amount was, how much was applied to your deductible, and how much your insurer is reimbursing you.

Understanding the Financial Math of Out of Network Therapy

Understanding the actual financial calculation helps you estimate your real out of pocket cost before committing to out of network therapy. Here is how the math works.

Your therapist charges $200 per session. Your insurance plan’s allowed amount for outpatient psychotherapy is $120. Your out of network deductible is $500 and you have not met any of it. Your coinsurance after deductible is 40 percent.

For the first several sessions, your entire $120 allowed amount applies to your $500 deductible. After about 4 sessions your deductible is met. After that, insurance pays 60 percent of the $120 allowed amount ($72) and you pay 40 percent ($48) plus the $80 difference between the allowed amount and the therapist’s actual charge. Your net cost per session after deductible is met: $128 out of pocket ($48 coinsurance plus $80 difference). Your reimbursement: $72 per session.

This calculation makes clear why verifying the allowed amount and your specific coinsurance percentage matters before starting out of network therapy.

When Out of Network Therapy Is Worth the Extra Cost

Out of network therapy is particularly valuable in several situations. When the therapist best suited to your specific needs, diagnosis, or treatment preferences is not in your network. When in-network therapists in your area are not accepting new patients and the wait for in-network care is several months. When you have already established a strong therapeutic relationship with an out of network therapist and the disruption of changing providers would harm your treatment. When your specific mental health condition benefits from a specialized therapy approach that few in-network providers offer.

The quality of the therapeutic relationship and the fit between you and your therapist are among the strongest predictors of therapy outcomes. A great out of network therapist who truly understands your needs may produce better treatment results than an available in-network therapist who is not the right match — making the additional cost worthwhile in both financial and treatment terms.

Common Out of Network Reimbursement Problems and How to Solve Them

Claim denied for missing information: Ensure the superbill contains all required elements, particularly the NPI number and diagnosis code. Missing information is the most common reason for initial denials. Contact your therapist to provide a corrected superbill and resubmit.

Reimbursement lower than expected: Verify that the allowed amount your insurer used matches what they told you when you called before starting therapy. If the amounts differ, call member services and request an explanation. Sometimes the allowed amount depends on the specific CPT code billed, which may differ from what you were quoted.

Diagnosis code not covered: Some insurance plans exclude coverage for certain diagnosis codes. If your therapist’s diagnosis does not match a covered category, discuss with your therapist whether an alternative accurate diagnosis code may be more appropriate clinically. If a denial seems incorrect, follow the appeal process described in our guide on How to Appeal a Therapy Insurance Denial.

Frequently Asked Questions About Out of Network Therapy

Does my out of network deductible count toward my in-network deductible? In some plans yes, in others they are separate. Check your plan documents — it will specify whether you have a combined or separate deductible for in-network and out of network care.

Can I use out of network benefits for telehealth therapy? Generally yes. Most plans that cover out of network in-person therapy also cover telehealth with an out of network provider. Verify the specific telehealth rules with your insurer. For more on telehealth coverage, see our guide on Telehealth Therapy and Insurance Coverage.

How far back can I submit out of network claims? Most insurers have a timely filing deadline of 90 to 180 days from the date of service. Check your plan documents for the specific deadline and submit claims promptly to avoid denial for late filing.

Do I need a referral for out of network therapy? This depends on your plan type. PPO plans typically do not require referrals. POS and HMO plans often do. Check with your insurer before your first appointment.

Conclusion

Out of network therapy benefits, while requiring more administrative effort than in-network care, provide access to the full range of licensed therapists rather than only those contracted with your insurance company. By understanding how superbills work, what questions to ask your insurer before starting, and how the financial calculation works, you can make an informed decision about whether out of network therapy makes sense for your situation and budget. Combined with the information in our guides on How to Find a Therapist That Takes Your Insurance and What is a Therapy Copay, this knowledge gives you a complete picture of your mental health insurance options.