Does Insurance Cover Therapy? Complete Guide to Mental Health Benefits in 2026

Does Insurance Cover Therapy? Complete Guide to Mental Health Benefits in 2026

If you have ever considered therapy but worried about the cost, you are not alone. Mental health care can be expensive, and navigating insurance coverage adds another layer of confusion to an already difficult process. The good news is that most insurance plans in the United States are required by law to cover mental health services — and understanding your benefits can save you hundreds or thousands of dollars per year.

This guide answers every question you might have about insurance coverage for therapy, from what types of therapy are covered to how to find in-network providers and what to do if your claim is denied.

The Short Answer: Yes, Insurance Usually Covers Therapy

Thanks to the Mental Health Parity and Addiction Equity Act (MHPAEA) and the Affordable Care Act (ACA), most health insurance plans are required to cover mental health services at the same level as physical health services. This means if your plan covers doctor visits with a copay, it must cover therapy visits with a comparable copay.

Mental health benefits typically include individual therapy, group therapy, family and couples therapy (varies by plan), psychiatric evaluation and medication management, substance use disorder treatment, and inpatient mental health hospitalization. The specific coverage, costs, and rules vary significantly between insurance plans, which is why understanding your particular benefits is essential.

Types of Insurance That Cover Therapy

Employer-sponsored health insurance: Most employer plans cover mental health services. Large employer plans are subject to MHPAEA requirements. Check your Summary of Benefits and Coverage document for mental health specifics.

Marketplace (ACA) plans: All plans sold on HealthCare.gov and state marketplaces are required to cover mental health and substance use disorder services as one of the 10 Essential Health Benefits. Coverage must be comparable to medical and surgical benefits.

Medicaid: Medicaid covers a broad range of mental health services for eligible low-income individuals. Coverage varies by state, but all states must cover basic mental health services.

Medicare: Medicare Part B covers outpatient mental health services including psychotherapy and psychiatric evaluation. Medicare pays 80% of the approved amount after you meet your Part B deductible; you pay the remaining 20%.

CHIP: Children’s Health Insurance Program covers mental health services for eligible children and teens in families that earn too much for Medicaid.

Short-term health plans and some grandfathered plans: These may not be required to cover mental health services. Read the plan documents carefully if you have one of these plans.

What You Will Typically Pay for Therapy With Insurance

Your actual cost depends on several factors in your insurance plan:

Deductible: The amount you pay out of pocket before insurance starts paying. If you have a $1,500 deductible, you pay the full cost of therapy sessions until you have paid $1,500 in covered services for the year. Therapy sessions typically cost $100 to $200 each without insurance, so you might pay full cost for 8 to 15 sessions before your deductible is met.

Copay: A fixed amount you pay per therapy session after meeting your deductible. Common copays for mental health visits are $20 to $60.

Coinsurance: Instead of a fixed copay, some plans charge a percentage. For example, you might pay 20% of the therapy cost after your deductible, with insurance covering the remaining 80%.

Out-of-pocket maximum: The maximum amount you will pay in a year before insurance covers 100% of covered services. Once you hit this limit, therapy sessions are fully covered. Limits typically range from $3,000 to $8,700.

In-Network vs. Out-of-Network Therapists

This distinction is one of the most important cost factors in therapy coverage:

In-network therapists have contracted with your insurance company to accept negotiated rates. When you see an in-network therapist, you pay your copay or coinsurance, and insurance pays the rest. This is by far the least expensive option.

Out-of-network therapists have not contracted with your insurance company. Your plan may still cover out-of-network therapy, but at a much higher cost to you. You might pay 40% to 50% of the bill, or even the full amount if your plan has no out-of-network mental health benefits.

Always verify a therapist is in-network before your first appointment. You can check your insurer’s online provider directory, call the therapist’s office directly and ask them to verify your coverage, or call the member services number on your insurance card.

How to Find an In-Network Therapist

Finding an in-network therapist can be frustratingly difficult. Provider directories are often outdated, and many listed therapists are not actually accepting new patients. Here is a systematic approach:

Start with your insurance company’s online provider directory. Search for therapists in your area with your specific plan. Call the therapist’s office and ask: “Are you currently accepting new patients? Do you accept [Insurance Company] [Plan Name]?” Get a specific answer — “we accept most insurance” is not enough.

Online therapy platforms like Talkspace and BetterHelp accept many insurance plans and offer faster access to therapists than traditional in-person practice. Many people can get their first appointment within days rather than the weeks or months often required for in-person therapists.

Psychology Today’s therapist finder (psychologytoday.com/us/therapists) lets you filter by insurance accepted and specialty. It is one of the most comprehensive therapist directories available.

Understanding Your Explanation of Benefits (EOB)

After each therapy session, your insurance company will send an Explanation of Benefits — a document explaining what was billed, what insurance paid, and what you owe. Review your EOB carefully after each session to ensure charges are accurate. Key things to check: the date of service matches when you actually saw the therapist, the procedure code (CPT code) is correct, the amount billed matches what your therapist charges, and the amount you owe matches your copay or deductible calculation.

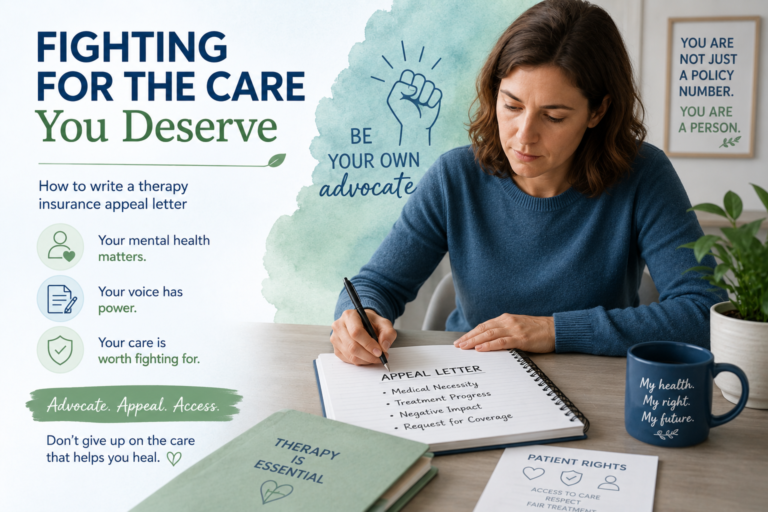

What If Your Insurance Denies a Therapy Claim?

Claim denials are frustratingly common in mental health care, but they are often reversible. You have the right to appeal a denial. Common reasons for denial include: the therapist is out of network, the service is deemed not medically necessary, the CPT code was entered incorrectly, or prior authorization was required but not obtained.

When appealing, request the specific reason for denial in writing. Gather supporting documentation from your therapist including a letter of medical necessity. File your appeal within the deadline specified in the denial letter (usually 30 to 180 days). If your internal appeal is denied, you may have the right to an external review by an independent organization.

Options When Insurance Does Not Cover Enough

If your insurance coverage for therapy is inadequate or you cannot find an in-network therapist, these options can help reduce costs:

Sliding scale fees: Many therapists offer fees based on income. Ask directly — “Do you offer sliding scale fees?” Many therapists who do not advertise this will accommodate it if asked.

Community mental health centers: Federally funded community mental health centers provide services on a sliding scale based on income. Find one at samhsa.gov/find-help.

University training clinics: Universities with psychology programs often offer therapy at reduced rates provided by supervised graduate students.

Open Path Collective: A network of therapists who offer sessions at $30 to $80 for individuals without insurance or with high out-of-pocket costs.

Employee Assistance Programs (EAP): Many employers offer EAPs that provide a certain number of free therapy sessions per year. Check with your HR department.

Online Therapy and Insurance

Telehealth therapy — therapy via video call — expanded dramatically during the pandemic and has remained popular. Most insurance plans now cover telehealth mental health services at the same rate as in-person visits. Platforms like Talkspace, Teladoc, and MDLive accept many insurance plans and offer more appointment availability than traditional practices.

Take the First Step

If you have been putting off therapy because of cost concerns, take 15 minutes today to call the member services number on your insurance card and ask specifically about your mental health benefits. Understanding your coverage removes a major barrier to getting the help you deserve. You have paid for these benefits — use them.